Between September and December, the so-called US big three carriers—American Airlines, Delta Air Lines, and United Airlines—collectively plan 917 daily international departures (double for both ways). They will operate 41% of the country’s international services. These findings are from analyzing the latest Cirium Diio data.

United has the most departures of the trio, mainly due to its strong long-haul presence, although it doesn’t yet plan any never-before-served European flights next year. American is very close (346), largely because of its extensive operations, particularly to Mexico, the Caribbean, and South America. Delta is in distant third place (220).

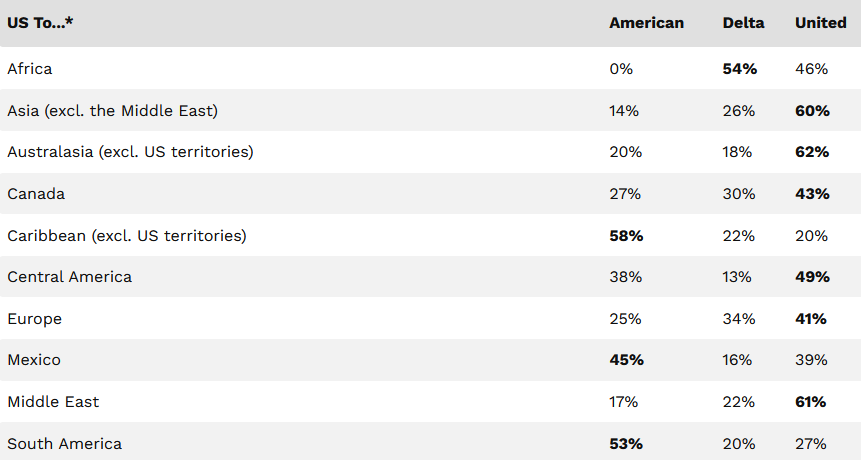

Where Each Carrier Is More Dominant Internationally

The following table provides market shares (based on September-December flights) for each of the three US operators across different geographies. The percentages relate only to nonstop flights provided by American, Delta, or United. They do not consider services by foreign carriers, even joint venture partners or alliance members, which could change things significantly in some instances.

With only one exception, the three carriers have flights to all ten examined continents, regions, and specific countries. American’s frames do not fly to Africa. However, in 2019, the oneworld member announced plans to fly the now-retired Boeing 757 from Philadelphia (where it has 75% of the services) to Casablanca. The coronavirus pandemic put paid to that idea. Since then, it has not publicly stated its desire to commence service to Morocco.

Here is a fact-based summary of the story contents:

Between September and December, the so-called US big three carriers—American Airlines, Delta Air Lines, and United Airlines—collectively plan 917 daily international departures (double for both ways). They will operate 41% of the country’s international services. These findings are from analyzing the latest Cirium Diio data.

With 351 daily departures, United has the most departures of the trio, mainly due to its strong long-haul presence, although it doesn’t yet plan any never-before-served European flights next year. American is very close (346), largely because of its extensive operations, particularly to Mexico, the Caribbean, and South America. Delta is in distant third place (220).

Where Each Carrier Is More Dominant Internationally

The following table provides market shares (based on September-December flights) for each of the three US operators across different geographies. The percentages relate only to nonstop flights provided by American, Delta, or United. They do not consider services by foreign carriers, even joint venture partners or alliance members, which could change things significantly in some instances.

With only one exception, the three carriers have flights to all ten examined continents, regions, and specific countries. American’s frames do not fly to Africa. However, in 2019, the oneworld member announced plans to fly the now-retired Boeing 757 from Philadelphia (where it has 75% of the services) to Casablanca. The coronavirus pandemic put paid to that idea. Since then, it has not publicly stated its desire to commence service to Morocco.

| US To…* | American | Delta | United |

|---|---|---|---|

| Africa | 0% | 54% | 46% |

| Asia (excl. the Middle East) | 14% | 26% | 60% |

| Australasia (excl. US territories) | 20% | 18% | 62% |

| Canada | 27% | 30% | 43% |

| Caribbean (excl. US territories) | 58% | 22% | 20% |

| Central America | 38% | 13% | 49% |

| Europe | 25% | 34% | 41% |

| Mexico | 45% | 16% | 39% |

| Middle East | 17% | 22% | 61% |

| South America | 53% | 20% | 27% |

| * Asia and the Middle East are treated separately for clarity |

United is #1 In 6 Of The 10 Markets

Compared to American and Delta, United is the number one operator to Asia (excluding the Middle East), Australasia, Canada, Central America, Europe, and the Middle East. The gap between the Star Alliance carrier and the second-largest US big three operator is greatest to Australasia. United has a 62% share against just 20% for American.

Of particular note is United’s new route from San Francisco to Adelaide, with a three-weekly Boeing 787-9 service beginning on December 11. It will become the carrier’s fourth Australian city, and the first time the South Australian capital has ever had nonstop US flights.

Cirium shows that United is the largest of all airlines (US and foreign) to half of these six areas. The exceptions are Canada (it is second to Air Canada), Central America (it is second to Copa), and the Middle East (it is fifth, behind Qatar Airways, Emirates, El Al, and Etihad). Of course, it partners with some of these carriers.Compared to American and Delta, United is the number one operator to Asia (excluding the Middle East), Australasia, Canada, Central America, Europe, and the Middle East. The gap between the Star Alliance carrier and the second-largest US big three operator is greatest to Australasia. United has a 62% share against just 20% for American.

Of particular note is United’s new route from San Francisco to Adelaide, with a three-weekly Boeing 787-9 service beginning on December 11. It will become the carrier’s fourth Australian city, and the first time the South Australian capital has ever had nonstop US flights.

Cirium shows that United is the largest of all airlines (US and foreign) to half of these six areas. The exceptions are Canada (it is second to Air Canada), Central America (it is second to Copa), and the Middle East (it is fifth, behind Qatar Airways, Emirates, El Al, and Etihad). Of course, it partners with some of these carriers.

Delta Is Only #1 To Africa

Delta is only dominant to Africa, which is partly because American doesn’t fly there. Delta has eight routes to Africa,two of which are either new or returning this year: Atlanta to Accra (resuming on December 1; last served in 2012), Cape Town, Johannesburg, Lagos, and Marrakech (beginning on October 25), along with New York JFK to Accra, Dakar, and Lagos.

Delta ranks second to Asia (excluding the Middle East), Canada, the Caribbean, Europe, and the Middle East (helped by the return of Tel Aviv flights on September 1). Some of these markets particularly rely on SkyTeam’s strong prominence, particularly Delta’s many flights to Amsterdam, Paris CDG, and Seoul Incheon hubs.

{kind=link}